The first is coming from Cobra, here is the summary:

- Usually a bottom is not in place before VIX forms a reversal candle (e.g., black candle, Doji, etc), from this perspective the Friday low may not be a bottom. What about next Monday? There is a pattern recently, once it repeats the market should rise. Will be the third time different? I don't know.

SPY Short-term Trading Signals

Friday hollow red candle appears, then the next Monday opens high closes higher. In the past the third time is often different. So it is unknown how it goes this time.

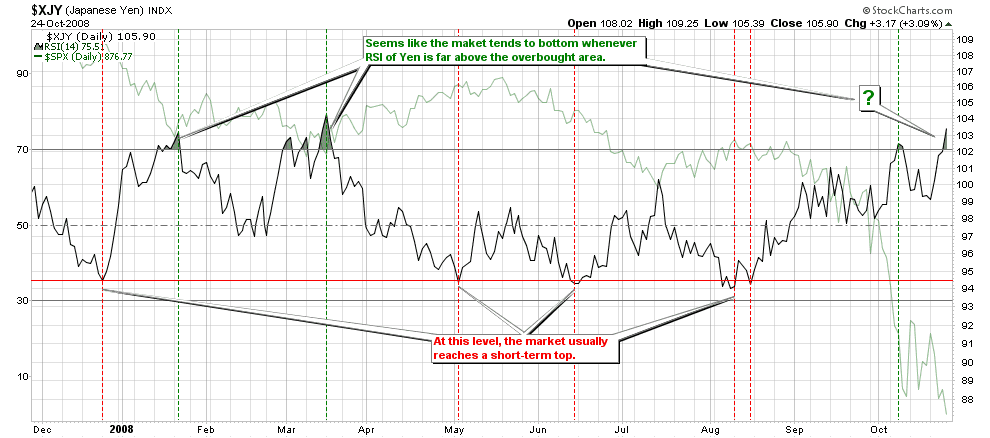

Yen RSI and the Market Top/Bottom

Every time the RSI of YEN reaches overbought region, the market is close to a bottom or has a big rally. Now it is overbought again, and this is obviously a good news.

The second is coming from The Headline Charts, here is the summary:

- If the end of the world were around the corner, people would be buying Treasuries to the point where rates would be hitting new lows. Instead, each push lower by stocks has produced higher rates, and this is a good sign that markets are healing, and flight to safety is easing.

I know, you worry about the health of the US government longer-term, and for many reasons. Me too. But for now, let's worry about this bear market for stocks and commodities, and look for good signs that the crisis stage of the bear has peaked. This is the best sign so far.

We've been looking for signs that we are emerging from the capital preservation stage which occurs at the end of the cycle, and to the next stage. I think this graph is missing a phase, which is the phase we are entering. I think we have now probably passed into the late contraction part of the cycle where the yield curve is very steep, and emotion settles down from panic to a level of pessimism and "why bother".

At this stage all the money flows to fixed instruments of short maturities with very low yields, like CDs. In fact, I think we should now (or maybe early next year) expect to start seeing CD rates generally ease as banks get close to having built up their cash positions again, and don't need to attract new money as much as they did.

- Why the dollar is rising?

A number of analysts had predicted the continued demise of the US dollar thanks to the financial-sector bailout and weakening economy but its sharp upside has surprised many. The dollar's recent climb is part of a massive reversal of long-standing investing trends (due to the global economic slowdown) such as buying emerging-market stocks or wagering on rising commodity prices. When investors retreat from such investments, they are often selling them in exchange for US dollars. The U.S. currency remains the most popular among global institutions, accounting for 55% of the assets and liabilities they hold in foreign currencies, according to the Bank for International Settlements. It has been further boosted because banks around the world are scrambling for dollars after inter-bank borrowing between banks all but ceased to function during the past month thanks to the liquidity crunch

After sending money overseas for years, U.S. investors now are bringing it home in a flight to safety. In July and August, the latest months for which Treasury Department data are available, U.S. investors sold $57 billion more in foreign stocks and bonds than they bought -- the largest-ever such repatriation. Dollar demand has also been reflected in the rise in purchases (and hence the price) of U.S. Treasury bonds, seen as the safest haven of all. The most recent data shows that such holdings of Treasury's increased by about $100 billion over the past four weeks. Other countries are also feeling the effects (even more than the US) and so are slashing interest rates to try and boost domestic economic activity, so the expected yield differential with the US is falling. With this trend set to continue, investors will continue to flock to the dollar.

The US economy is likely to recover faster than other economies because unlike other central banks, the Fed more than a year ago began lowering interest rates, which punished the dollar. Now it could be a positive, as other central banks catch up. In the U.S., "a lot of the heavy lifting has already been put in the pipeline," says Stephen Jen, global head of currency strategy at Morgan Stanley, in the WSJ. "The same cannot be said of Europe." The same old reasoning still applies: The U.S. is regarded as being able to weather a recession much better than the euro zone

As the dollar rises, US consumers are seeing some clear benefits which overall should boost spending and assist with getting the nation out the current economic slump. Benefits of the high US dollar to every day consumers include, lower oil and commodity prices, lower inflation (prices) and cheaper travel. It does hurt foreign corporate profits and exporters, but given our economy is 70% consumer driven, I think what helps consumers is much more important right now.

Given the rapid rise in the dollar in synchronization with the escalation of the global financial meltdown and tightening credit markets, it stands to reason that as credit and stock markets stabilize so too will the dollar. This means it will give back some of its gains, but should be able to maintain current levels well into next year. If the government implements much needed long term regulatory reform and adopts a more fiscally conservative policy once the economy has recovered, then there is a chance that the US dollar could maintain its strength for a number of years to come.

The fourth is coming from Kathy Lien, here is the summary:

- The mentality in the currency and stock markets is sell now, ask questions later. The low yielding US dollar and Japanese Yen continue to be the biggest beneficiaries of risk aversion. The only thing that investors want right now are safe haven plays. The dollar’s strength will force emerging market countries to rush to prevent a flight of capital out of their currencies - more rate hikes could be likely. With deleveraging being the theme of the day, when confidence is lost, it will be difficult to recover.

Where are the Value Points for the Currency Market?

In the Wed edition of my Daily GFT Report and on CNBC and Bloomberg I talked about how the dollar could rise another 5%. At that time, the EUR/USD was trading at 1.2829 and the GBP/USD at 1.6236. The GBP/USD has already hit my 5 percent target and at one point this morning even became undervalued on a purchasing parity basis. Although the UK GDP report confirms that the country is headed for a recession and validates the weakness, I believe that we have seen a near term low in the currency pair.

The EUR/USD on the other hand has only dropped 2.5 percent. The EUR/USD does not become a value play until 1.15-1.20. As for USD/JPY, it has also reached my target of 95. Although I won’t be a buyer at these levels, I won’t be a seller either. There are no rewards for heros in this type of market.

And the last is coming from Barry Ritholtz, see: 10/24/2008 Market Recap - Global Investors Retreat (Update 2)

Related Posts :

- 10/24/2008 Market Recap - Global Investors Retreat (Update 2)

- 10/23/2008 - October Blues

- Trading in the panic mode, futures halted

- Markets are in absolute freefall

- 10/23/2008 Market Recap-US Flat, Asian Sink

- Cobra's Market View: 10/24/2008 Market Recap: Descending Triangle, October 26, 2008

- Headlinecharts blog: Good Signal from Rates, October 25, 2008

- Saving to invest blog: US Dollar Rising and Outlook, October 23, 2008

- Kathy Lien: Dollar Closing In on 5% Targets, Where are the Value Points?, October 24, 2008

This is generally never true. Before buying or selling any stock you should do your own research and reach your own conclusion. See my Disclaimer on the bottom for more information.

You are welcome to republish this article, or any portion thereof.

Please, cite the actual/original source. I would be grateful if you could link back.